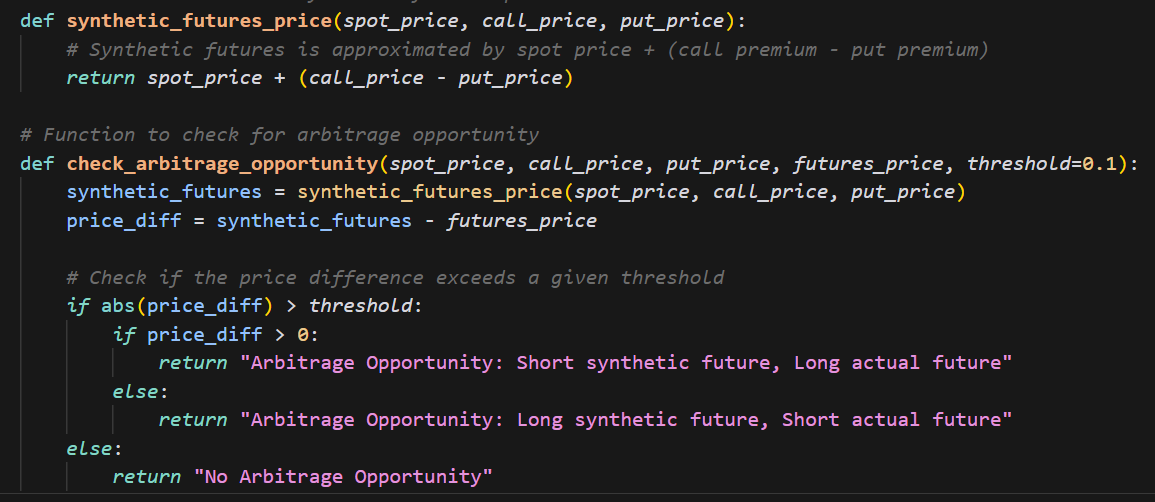

Hi Team, Here is my function for calculating Arbitrage opportunity basis put call parity theory. But i am unable for find code for future price of underline. I am using below code for future price which seems wrong. and code arbitrage.

Thanks Sathesh, Can we make it dynamic as if i need to see Arbitrage opportunity in 50 scripts, how would i do? It is difficult to right ACC JAN FUT, ITI JAN FUT and so on for each script to see the arbitrage opportunity.