Hi Imran Sir,

As discussed in the class, Please give tested code for calculating ROC.

Reminder!

Can we please have tested code? My strategy is on hold because of this.

Regards, Sobhit

Hi @Sobhit ,

We have started working on this, will let you know once done.

Hi @Sobhit

Check below Tested code

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as ta

import pytz

client_code =

token_id =

tsl = Tradehull(client_code,token_id)

ce_symbol_name, pe_symbol_name, strike_price = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

last_candle_time = datetime.datetime.now()

last_candle_time = last_candle_time.replace(hour=9, minute=15, second=0, microsecond=0)

ce_data = tsl.get_historical_data(tradingsymbol = ce_symbol_name,exchange = 'NFO',timeframe="1")

pe_data = tsl.get_historical_data(tradingsymbol = pe_symbol_name,exchange = 'NFO',timeframe="1")

print(ce_symbol_name)

print(pe_symbol_name)

while True:

candle_is_still_running = datetime.datetime.now() < last_candle_time + datetime.timedelta(minutes=1)

if candle_is_still_running is False:

ce_data = tsl.get_historical_data(tradingsymbol = ce_symbol_name,exchange = 'NFO',timeframe="1")

pe_data = tsl.get_historical_data(tradingsymbol = pe_symbol_name,exchange = 'NFO',timeframe="1")

last_candle_time = ce_data.iloc[-1]['timestamp'].to_pydatetime().replace(tzinfo=None)

continue

all_ltp_data = tsl.get_ltp_data(names=[ce_symbol_name, pe_symbol_name])

if candle_is_still_running:

ce_ltp = all_ltp_data[ce_symbol_name]

ce_data.iloc[-1, ce_data.columns.get_loc('close')] = ce_ltp

pe_ltp = all_ltp_data[pe_symbol_name]

pe_data.iloc[-1, pe_data.columns.get_loc('close')] = pe_ltp

merged_df = pd.merge(ce_data[['timestamp', 'close']], pe_data[['timestamp', 'close']], on='timestamp', suffixes=('_ce', '_pe')).set_index('timestamp')

merged_df['combined_premium'] = merged_df['close_ce'] + merged_df['close_pe']

merged_df['ROC'] = talib.ROC(merged_df['combined_premium'], timeperiod=10)

print(f"ce_ltp {ce_ltp}")

print(f"pe_ltp {pe_ltp}")

print(merged_df.tail())

Thanks for sharing the code, it is appreciated. Now my ask is that here we are calling historical data every minute, What will be the code, if i want to see data updating live (current date, combined ltp, current strike, ROC and Supertrend) on every tick but my trade entry should be on 3 min candle close. Please check my trade condition and confirm if it is good to go.

merged_df = pd.DataFrame({

'value': [10, 20, 30, 40, 50, 60, 70, 80, 90],

'time': [

'2025-01-30 09:10:00', '2025-01-30 09:15:00', '2025-01-30 09:16:00',

'2025-01-30 09:17:00', '2025-01-30 09:18:00', '2025-01-30 09:19:00',

'2025-01-30 09:20:00', '2025-01-30 09:25:00', '2025-01-30 09:30:00'

]

})

merged_df['time'] = pd.to_datetime(merged_df['time'])

merged_df.set_index('time', inplace=True)

# Get the first candle (9:15-9:18) and last candle

first_candle_mask = merged_df.index.time.between(datetime.time(9, 15), datetime.time(9, 18))

# Check and fetch values

if first_candle_mask.any():

First_cc, cc = merged_df[first_candle_mask].iloc[0], merged_df.iloc[-1]

print(f"First candle: {First_cc}\nLast candle: {cc}")

else:

print("No data for the first candle range (9:15-9:18)")

In this case we can call 3 min Historical data and update it every second…

Hi Imran Sir, Can you please check my full code and give tested code for my strategy.

Also, suggest where i was wrong.

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as ta

import xlwings as xw

import pytz

book = xw.Book("Straddle.xlsx")

Straddle_chart = book.sheets['Straddle Chart']

config_sheet = book.sheets['Config']

running_orders_sheet = book.sheets['Running Orders']

completed_orders_sheet = book.sheets['Completed Orders']

# Initialize client and connection

client_code = "1100889055"

token_id = "eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzUxMiJ9.eyJpc3MiOiJkaGFuIiwicGFydG5lcklkIjoiIiwiZXhwIjoxNzM5MDk5MTc3LCJ0b2DetlbkNvbnN1bWVyVHlwZSI6IlNFTEYiLCJ3ZWJob29rVXJsIjoiIiwiZGhhbkNsaWVudElkIjoiMTEwMDg4OTA1NSJ9.bX2eeT5ZMHh689KIp_3dUzRzbohivQvgAkrbjZonf2tTq6c4soTcMqnlP6gR4wOIVY1ctBSu_tL4_T51kcFyTA"

tsl = Tradehull(client_code, token_id)

single_order = {'Option name': None,'entry_strike': None,'date': None,'entry_time': None, 'ce_entry_price': None, 'pe_entry_price': None, 'buy_sell': None, 'qty': None, 'sl': None, 'exit_time': None, 'exit_price': None, 'pnl': None, 'remark': None, 'traded': None}

orderbook = {}

completed_orders = {'Option name': None,'entry_strike': None, 'date': None, 'entry_time': None, 'ce_entry_price': None, 'pe_entry_price': None, 'buy_sell': None, 'qty': None, 'sl': None, 'exit_time': None, 'exit_price': None, 'pnl': None, 'remark': None, 'traded': None}

watchlist = ['NIFTY']

all_dataframes = []

completed_orders = []

reentry = "yes" #"yes/no"

# Initialize merged_df outside the if block

merged_df = None

# Initialize Supertrend outside the if block

Supertrend = None

ce_name, pe_name, strike_price = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

last_candle_time = datetime.datetime.now()

last_candle_time = last_candle_time.replace(hour=9, minute=15, second=0, microsecond=0)

ce_data = tsl.get_historical_data(tradingsymbol=ce_name, exchange='NFO', timeframe="1")

pe_data = tsl.get_historical_data(tradingsymbol=pe_name, exchange='NFO', timeframe="1")

print(ce_name)

print(pe_name)

bot_token = "8009492753:AAEOEVp5v86ce4jcJuNXnv0_AAT4JfzNPGA"

receiver_chat_id = "876625569"

for name in watchlist:

orderbook[name] = single_order.copy()

while True:

print("starting while Loop \n\n")

current_time = datetime.datetime.now().time()

if current_time < datetime.time(13, 55):

print(f"Wait for market to start", current_time)

time.sleep(1)

continue

if current_time > datetime.time(23, 15):

order_details = tsl.cancel_all_orders()

print(f"Market over Closing all trades !! Bye Bye See you Tomorrow", current_time)

pdb.set_trace()

break

for name in watchlist:

# ------------------------------------- UPDATE SHEET -------------------------------------

try:

# Convert orderbook to DataFrame with explicit index

orderbook_df = pd.DataFrame.from_dict(orderbook, orient='index').reset_index()

running_orders_sheet.range('A1').value = orderbook_df

completed_orders_df = pd.DataFrame(completed_orders)

completed_orders_sheet.range('A1').value = completed_orders_df

except Exception as e:

print("Error in updating running orders sheet", e)

# ------------------------------------- GET DATA -------------------------------------

candle_is_still_running = datetime.datetime.now() < last_candle_time + datetime.timedelta(minutes=1)

ce_name, pe_name, strike_price = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

if candle_is_still_running is False:

ce_data = tsl.get_historical_data(tradingsymbol = ce_name,exchange = 'NFO',timeframe="1")

pe_data = tsl.get_historical_data(tradingsymbol = pe_name,exchange = 'NFO',timeframe="1")

last_candle_time = ce_data.iloc[-1]['timestamp'].to_pydatetime().replace(tzinfo=None)

continue

all_ltp_data = tsl.get_ltp_data(names=[ce_name, pe_name])

if candle_is_still_running:

ce_ltp = all_ltp_data[ce_name]

ce_data.iloc[-1, ce_data.columns.get_loc('close')] = ce_ltp

pe_ltp = all_ltp_data[pe_name]

pe_data.iloc[-1, pe_data.columns.get_loc('close')] = pe_ltp

merged_df = pd.merge(ce_data[['timestamp', 'close']], pe_data[['timestamp', 'close']], on='timestamp', suffixes=('_ce', '_pe')).set_index('timestamp')

merged_df['combined_premium'] = merged_df['close_ce'] + merged_df['close_pe']

# Calculate OHLC for combined premium

merged_df['combined_premium_high'] = merged_df['combined_premium'].rolling(window=1).max()

merged_df['combined_premium_low'] = merged_df['combined_premium'].rolling(window=1).min()

merged_df['combined_premium_open'] = merged_df['combined_premium'].shift(1)

merged_df['combined_premium_close'] = merged_df['combined_premium']

merged_df['ROC'] = talib.ROC(merged_df['combined_premium'], timeperiod=9)

# Calculate Supertrend using pandas_ta

Supertrend = ta.supertrend(merged_df['combined_premium_high'], merged_df['combined_premium_low'], merged_df['combined_premium_close'], 10, 2)

merged_df = pd.concat([merged_df, Supertrend], axis=1, join='inner')

# Remove .values from numpy float values since they don't have that attribute

combined_premium_value = merged_df['combined_premium'].iloc[-1]

roc_value = merged_df['ROC'].iloc[-1]

supertrend_value = Supertrend['SUPERTd_10_2.0'].iloc[-1]

data_to_write = [str(current_time), combined_premium_value, strike_price, roc_value, supertrend_value]

print(f"ce_ltp {ce_ltp}")

print(f"pe_ltp {pe_ltp}")

print(f'Supertrend {supertrend_value}')

last_row = 2

while Straddle_chart.range(f'A{last_row}').value is not None:

last_row += 1

if last_row > 30000: # Safety limit

last_row = 2 # Reset to top if sheet is full

break

# Add strike change message if strike price changed

if last_row > 2 and Straddle_chart.range(f'C{last_row-1}').value != strike_price:

data_to_write.append("Strike change to " + str(strike_price))

print(f"Strike price changed from {Straddle_chart.range(f'C{last_row-1}').value} to {strike_price}")

else:

data_to_write.append("")

Straddle_chart.range(f'A{last_row}:E{last_row}').value = data_to_write

# Initialize variables with default values before try block

tc1 = tc2 = tc3 = False

try:

# Get first and current candle for 3-minute timeframe

First_cc = merged_df.iloc[0] # First candle of 1-min period

cc = merged_df.iloc[-1] # Current candle of 1-min period

# Check if we're at the 3-min candle close

current_minute = current_time.minute

if current_minute % 3 != 0: # Only take trade at 3-min candle close

continue

tc1 = Supertrend['SUPERTd_10_2.0'].values[-1] == -1

tc2 = current_time > datetime.time(9, 15) and current_time < datetime.time(23, 15)

tc3 = orderbook[name]['traded'] is None

except Exception as e:

print("Error accessing data:", e)

continue

# Add a check before using Supertrend

if Supertrend is not None:

ec1 = Supertrend['SUPERTd_10_2.0'].values[-1] == 1

else:

ec1 = False # or handle this case as needed

# Check if entry_strike exists before comparing

# Check if entry strike exists and has changed

ec2 = False

if orderbook[name]['traded'] == "yes" and 'entry_strike' in orderbook[name]:

entry_strike = orderbook[name]['entry_strike']

if entry_strike != strike_price:

print(f"ATM strike changed from {entry_strike} to {strike_price}")

ec2 = True

ec3 = current_time >= datetime.time(15, 15) # Exit at 3:15 PM

ec4 = orderbook[name]['traded'] == "yes" # Check if trade is active

if tc1 and tc2 and tc3:

print("Trade condition met. Placing order...Short Straddle")

margin_avialable = tsl.get_balance()

margin_required = 200000

if margin_avialable < margin_required:

print(f"Less margin, not taking order : margin_avialable is {margin_avialable} and margin_required is {margin_required} for {name}")

continue

orderbook[name]['name'] = name

orderbook[name]['date'] = str(current_time.date())

orderbook[name]['entry_time'] = str(current_time.time())[:8]

orderbook[name]['buy_sell'] = "SELL"

orderbook[name]['qty'] = ce_qty or pe_qty

try:

ce_lot_size = tsl.get_lot_size(tradingsymbol=ce_name)

pe_lot_size = tsl.get_lot_size(tradingsymbol=pe_name)

# Set the quantity to 1 lot for both CE and PE

ce_qty = ce_lot_size * 1

pe_qty = pe_lot_size * 1

ce_entry_ordrid = tsl.order_placement(tradingsymbol=ce_name, exchange='NFO', quantity=orderbook[name]['qty'], price=ce_ltp, trigger_price=0, order_type='MARKET', transaction_type='SELL', trade_type='MIS', after_market_order=True)

orderbook[name]['entry_price'] = all_ltp_data[ce_name]

pe_entry_ordrid = tsl.order_placement(tradingsymbol=pe_name, exchange='NFO', quantity=orderbook[name]['qty'], price=pe_ltp, trigger_price=0, order_type='MARKET', transaction_type='SELL', trade_type='MIS', after_market_order=True)

orderbook[name]['entry_price'] = all_ltp_data[pe_name]

orderbook[name]['ce_entry_ordrid'] = ce_entry_ordrid

orderbook[name]['pe_entry_ordrid'] = pe_entry_ordrid

orderbook[name]['entry_time'] = str(datetime.datetime.now().time())[:8]

orderbook[name]['entry_datetime'] = datetime.datetime.now()

orderbook[name]['traded'] = "yes"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"Entry_done {name} \n\n {message}"

tsl.send_telegram_alert(message=message,receiver_chat_id=receiver_chat_id,bot_token=bot_token)

except Exception as e:

print(f"Error placing orders: {str(e)}")

print(f"Traceback: {traceback.format_exc()}")

else:

print("Trade condition not met. Skipping entry.")

# ------------------------------------- Exit Condition -------------------------------------

if (ec1 or ec2 or ec3) and ec4:

print("Exit condition met. Closing straddle position...", strike_price)

try:

# Store exit details

current_trade = orderbook[name].copy()

orderbook[name]['ce_name'] = ce_name

orderbook[name]['pe_name'] = pe_name

orderbook[name]['buy_sell'] = "BUY"

orderbook[name]['date'] = str(datetime.datetime.now().date())

orderbook[name]['exit_time'] = str(datetime.datetime.now().time())[:8]

orderbook[name]['exit_datetime']= datetime.datetime.now()

orderbook[name]['qty'] = ce_qty or pe_qty

# Place sell orders to close straddle position

ce_exit_ordrid = tsl.order_placement(tradingsymbol=orderbook[name]['ce_name'], exchange='NFO', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='BUY', trade_type='MIS')

orderbook[name]['exit_price'] = all_ltp_data[ce_name]

pe_exit_ordrid = tsl.order_placement(tradingsymbol=orderbook[name]['pe_name'], exchange='NFO', quantity=orderbook[name]['qty'], price=0, trigger_price=0, order_type='MARKET', transaction_type='BUY', trade_type='MIS')

orderbook[name]['exit_price'] = all_ltp_data[pe_name]

# Store exit order IDs

orderbook[name]['ce_exit_ordrid'] = ce_exit_ordrid

orderbook[name]['pe_exit_ordrid'] = pe_exit_ordrid

orderbook[name]['traded'] = None # Reset traded status

except Exception as e:

print(f"Error closing straddle position: {str(e)}")

print(f"Traceback: {traceback.format_exc()}")

if orderbook[name]['traded'] == "yes":

sold = orderbook[name]['buy_sell'] == "SELL"

bought = orderbook[name]['buy_sell'] == "BUY"

if sold and bought:

orderbook[name]['pnl'] = (orderbook[name]['ce_entry_price'] - orderbook['name']['ce_exit_price']) * orderbook[name]['qty'] + (orderbook[name]['pe_entry_price'] - orderbook['name']['pe_exit_price']) * orderbook[name]['qty']

completed_orders.append(orderbook[name])

orderbook[name] = {x:None for x in orderbook[name]}

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = None

Hi @Sobhit

Do run the code and share the error screenshot faced.

Getting below error.

“ce_ltp 116.05

pe_ltp 144.3

Supertrend 1

Error accessing data: ‘NoneType’ object is not subscriptable

starting while Loop”

Also, please check why my running order book not getting updated, further, please check this part of my code if it is rightly written.

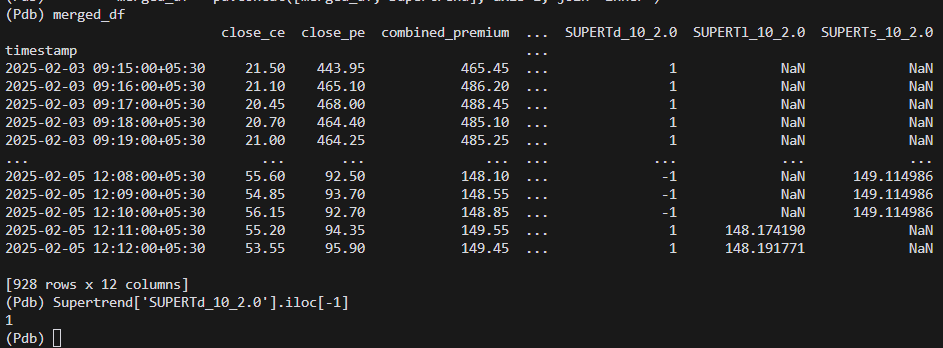

It seems the code is working fine to get the supertrend value:

Running orders will get updated only if orderbook_df is not empty

Code seems to be okay.

Can we call 3 minute historical data? Can you suggest the necessary changes in my code to take trade at 3 minutes candle close and exit the trade only at 3 minute candle close.

import pdb

import time

import datetime

import traceback

from Dhan_Tradehull import Tradehull

import pandas as pd

from pprint import pprint

import talib

import pandas_ta as ta

import xlwings as xw

import pytz

# Open the Excel workbook and necessary sheets

book = xw.Book("Straddle.xlsx")

Straddle_chart = book.sheets['Straddle Chart']

config_sheet = book.sheets['Config']

running_orders_sheet = book.sheets['Running Orders']

completed_orders_sheet = book.sheets['Completed Orders']

# Initialize client and connection

client_code = "11008890xx"

token_id = "eyJ0eXAiOiJKV1QiLCJhbGciOiJIUzUxMiJ9.eyJpc3MiOiJkaGFuIiwicGFydG5lcklkIjoiIiwiZXhwIjoxNzM5MDk5MTc3LCJ0b2tlbkNvbnNdhf1bWVyVHlwZSI6IlNFTEYiLCJ3ZWJob29rVXJsIjoiIiwiZGhhbkNsaWVudElkIjoiMTEwMDg4OTA1NSJ9.bX2eeT5ZMHh689KIp_3dUzRzbohivQvgAkrbjZonf2tTq6c4soTcMqnlP6gR4wOIVY1ctBSu_tL4_T51kcFyTA"

tsl = Tradehull(client_code, token_id)

# Define the order structure

single_order = {'Option name': None,'entry_strike': None,'date': None,'entry_time': None, 'ce_entry_price': None, 'pe_entry_price': None, 'combined_premium_entry_price': None, 'buy_sell': None, 'exit_time': None, 'ce_exit_price': None, 'pe_exit_price': None, 'combined_premium_exit_price': None,'ce_qty': None, 'pe_qty': None, 'pnl': None, 'remark': None, 'traded': None}

orderbook = {}

completed_orders = {'Option name': None,'entry_strike': None,'date': None,'entry_time': None, 'ce_entry_price': None, 'pe_entry_price': None, 'combined_premium_entry_price': None, 'buy_sell': None, 'exit_time': None, 'ce_exit_price': None, 'pe_exit_price': None, 'combined_premium_exit_price': None,'ce_qty': None, 'pe_qty': None, 'pnl': None, 'remark': None, 'traded': None}

watchlist = ['NIFTY']

all_dataframes = []

completed_orders = []

reentry = "yes" # "yes/no"

merged_df = None

Supertrend = None

# Initialize trading symbols

ce_name, pe_name, strike_price = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

last_candle_time = datetime.datetime.now().replace(hour=9, minute=15, second=0, microsecond=0)

# Initial data fetching

ce_data = tsl.get_historical_data(tradingsymbol=ce_name, exchange='NFO', timeframe="1")

pe_data = tsl.get_historical_data(tradingsymbol=pe_name, exchange='NFO', timeframe="1")

# Print the option names for debugging

print(ce_name)

print(pe_name)

# Telegram bot configuration for alerts

bot_token = "8009492753:AAEOEVp5v86ce4jcJuNXnv0_AAT4JfzNPGA"

receiver_chat_id = "876625569"

# Initialize the orderbook for each watchlist item

for name in watchlist:

orderbook[name] = single_order.copy()

# Main loop

while True:

print("starting while Loop \n\n")

current_time = datetime.datetime.now().time()

current_datetime = datetime.datetime.now()

if current_time < datetime.time(9, 15):

print(f"Wait for market to start", current_time)

time.sleep(60)

continue

if current_time > datetime.time(15, 25):

order_details = tsl.cancel_all_orders()

print(f"Market over Closing all trades !! Bye Bye See you Tomorrow", current_time)

pdb.set_trace()

break

# Check if 3-minute candle has closed

# Track 3-minute candle time

for name in watchlist:

try:

# Update the Excel sheets for running and completed orders

orderbook_df = pd.DataFrame.from_dict(orderbook, orient='index').reset_index()

# Convert DataFrame to a list of lists for Excel

orderbook_values = [orderbook_df.columns.tolist()] + orderbook_df.values.tolist()

running_orders_sheet.range('A1').value = orderbook_values

# Handle completed orders

if completed_orders: # Only update if there are completed orders

completed_orders_df = pd.DataFrame(completed_orders)

completed_values = [completed_orders_df.columns.tolist()] + completed_orders_df.values.tolist()

completed_orders_sheet.range('A1').value = completed_values

except Exception as e:

print(f"Error in updating Excel sheets: {str(e)}")

print(f"Traceback: {traceback.format_exc()}")

# Get new data

candle_is_still_running = datetime.datetime.now() < last_candle_time + datetime.timedelta(minutes=1)

ce_name, pe_name, strike_price = tsl.ATM_Strike_Selection(Underlying='NIFTY', Expiry=0)

if not candle_is_still_running:

ce_data = tsl.get_historical_data(tradingsymbol=ce_name, exchange='NFO', timeframe="1")

pe_data = tsl.get_historical_data(tradingsymbol=pe_name, exchange='NFO', timeframe="1")

last_candle_time = ce_data.iloc[-1]['timestamp'].to_pydatetime().replace(tzinfo=None)

continue

all_ltp_data = tsl.get_ltp_data(names=[ce_name, pe_name])

if candle_is_still_running:

ce_ltp = all_ltp_data[ce_name]

ce_data.iloc[-1, ce_data.columns.get_loc('close')] = ce_ltp

pe_ltp = all_ltp_data[pe_name]

pe_data.iloc[-1, pe_data.columns.get_loc('close')] = pe_ltp

merged_df = pd.merge(ce_data[['timestamp', 'close']], pe_data[['timestamp', 'close']], on='timestamp', suffixes=('_ce', '_pe')).set_index('timestamp')

merged_df['combined_premium'] = merged_df['close_ce'] + merged_df['close_pe']

merged_df['combined_premium_high'] = merged_df['combined_premium'].rolling(window=1).max()

merged_df['combined_premium_low'] = merged_df['combined_premium'].rolling(window=1).min()

merged_df['combined_premium_open'] = merged_df['combined_premium'].shift(1)

merged_df['combined_premium_close'] = merged_df['combined_premium']

merged_df['ROC'] = talib.ROC(merged_df['combined_premium'], timeperiod=9)

Supertrend = ta.supertrend(merged_df['combined_premium_high'], merged_df['combined_premium_low'], merged_df['combined_premium_close'], 10, 2)

merged_df = pd.concat([merged_df, Supertrend], axis=1, join='inner')

combined_premium_value = merged_df['combined_premium'].iloc[-1]

roc_value = merged_df['ROC'].iloc[-1]

supertrend_value = Supertrend['SUPERTd_10_2.0'].iloc[-1]

data_to_write = [str(current_time), combined_premium_value, strike_price, roc_value, supertrend_value]

print(f"ce_ltp {ce_ltp}")

print(f"pe_ltp {pe_ltp}")

print(f'Supertrend {supertrend_value}')

last_row = 2

while Straddle_chart.range(f'A{last_row}').value is not None:

last_row += 1

if last_row > 30000:

last_row = 2 # Reset to top if sheet is full

break

# Add strike change message if strike price changed

if last_row > 2 and Straddle_chart.range(f'C{last_row-1}').value != strike_price:

data_to_write.append("Strike change to " + str(strike_price))

print(f"Strike price changed from {Straddle_chart.range(f'C{last_row-1}').value} to {strike_price}")

else:

data_to_write.append("")

Straddle_chart.range(f'A{last_row}:E{last_row}').value = data_to_write

tc1 = Supertrend['SUPERTd_10_2.0'].iloc[-1] == -1

tc2 = current_time > datetime.time(9, 15) and current_time < datetime.time(23, 15)

tc3 = orderbook[name] and orderbook[name]['traded'] is None

# Trade conditions met - checking on 3 min timeframe

# Check if current time is at 3-minute candle close

current_minute = current_time.minute

check_conditions = False

if current_minute % 3 == 0 and current_time.second == 0:

check_conditions = True

print(f"Checking conditions at {current_time} - 3 min candle close")

if tc1 and tc2 and tc3 and check_conditions:

print("Trade condition met. Placing order...Short Straddle")

ce_lot_size = tsl.get_lot_size(tradingsymbol=ce_name)

pe_lot_size = tsl.get_lot_size(tradingsymbol=pe_name)

# Set the quantity to 1 lot for both CE and PE

ce_qty = ce_lot_size * 4

pe_qty = pe_lot_size * 4

orderbook[name]['Option name'] = name

orderbook[name]['entry_strike'] = strike_price

orderbook[name]['date'] = str(datetime.datetime.now().date())

orderbook[name]['buy_sell'] = "SELL"

orderbook[name]['ce_qty'] = ce_qty

orderbook[name]['pe_qty'] = pe_qty

try:

ce_entry_ordrid = 111111111

orderbook[name]['ce_entry_price'] = all_ltp_data[ce_name]

pe_entry_ordrid = 222222222

orderbook[name]['pe_entry_price'] = all_ltp_data[pe_name]

orderbook[name]['combined_premium_entry_price'] = all_ltp_data[ce_name] + all_ltp_data[pe_name]

orderbook[name]['ce_entry_ordrid'] = ce_entry_ordrid

orderbook[name]['pe_entry_ordrid'] = pe_entry_ordrid

orderbook[name]['entry_time'] = str(datetime.datetime.now().time())[:8]

orderbook[name]['traded'] = "yes"

message = "\n".join(f"'{key}': {repr(value)}" for key, value in orderbook[name].items())

message = f"Entry_done {name} \n\n {message}"

tsl.send_telegram_alert(message=message, receiver_chat_id=receiver_chat_id, bot_token=bot_token)

except Exception as e:

print(f"Error placing orders: {str(e)}")

print(f"Traceback: {traceback.format_exc()}")

else:

print("Trade condition not met. Skipping entry.")

# Exit conditions

ec1 = Supertrend['SUPERTd_10_2.0'].iloc[-1] == 1

ec2 = False

if orderbook[name]['entry_strike'] is not None:

ec2 = abs(orderbook[name]['entry_strike'] - strike_price) >= 50

ec3 = current_time >= datetime.time(23, 15)

ec4 = orderbook[name]['traded'] == "yes"

if (ec1 or ec2 or ec3) and ec4 and check_conditions:

print("Exit condition met. Closing straddle position...", "Reason:", "Supertrend == 1" if ec1 else "Strike Price Difference >= 50" if ec2 else "Time >= 23:15")

try:

# Store exit details

orderbook[name]['Option name'] = name

orderbook[name]['entry_strike'] = strike_price

orderbook[name]['buy_sell'] = "BUY"

orderbook[name]['date'] = str(datetime.datetime.now().date())

orderbook[name]['exit_time'] = str(datetime.datetime.now().time())[:8]

orderbook[name]['exit_datetime'] = datetime.datetime.now()

orderbook[name]['ce_qty'] = ce_qty

orderbook[name]['pe_qty'] = pe_qty

# Place sell orders to close straddle position

ce_exit_ordrid = 333333333

orderbook[name]['ce_exit_price'] = all_ltp_data[ce_name]

pe_exit_ordrid = 444444444

orderbook[name]['pe_exit_price'] = all_ltp_data[pe_name]

orderbook[name]['combined_premium_exit_price'] = all_ltp_data[ce_name] + all_ltp_data[pe_name]

orderbook[name]['ce_exit_ordrid'] = ce_exit_ordrid

orderbook[name]['pe_exit_ordrid'] = pe_exit_ordrid

orderbook[name]['traded'] = None # Reset traded status

# Calculate PnL after closing straddle position

ce_pnl = (orderbook[name]['ce_entry_price'] - orderbook[name]['ce_exit_price']) * orderbook[name]['ce_qty']

pe_pnl = (orderbook[name]['pe_entry_price'] - orderbook[name]['pe_exit_price']) * orderbook[name]['pe_qty']

total_pnl = ce_pnl + pe_pnl

orderbook[name]['pnl'] = total_pnl

# Send PnL alert

pnl_message = f"Trade closed for {name}\nEntry Strike: {orderbook[name]['entry_strike']}\nCE PnL: {ce_pnl:.2f}\nPE PnL: {pe_pnl:.2f}\nTotal PnL: {total_pnl:.2f}"

tsl.send_telegram_alert(message=pnl_message, receiver_chat_id=receiver_chat_id, bot_token=bot_token)

# Add to completed orders and reset orderbook

completed_orders.append(orderbook[name].copy())

orderbook[name] = single_order.copy()

except Exception as e:

print(f"Error closing straddle position: {str(e)}")

print(f"Traceback: {traceback.format_exc()}")

if reentry == "yes":

completed_orders.append(orderbook[name])

orderbook[name] = single_order.copy()

Hi @Sobhit ,

Currently, Dhan does not support 3-minute data. It only provides the following timeframes: ['1', '5', '15', '25', '60', 'DAY'].

So can’t i take trade on 3 minute candle close? If yes, what modification do i need to make in my trade entry and exit conditions?

Hi @Sobhit,

To use 3-minute candle data, you can use one minute data and resample the data using python.