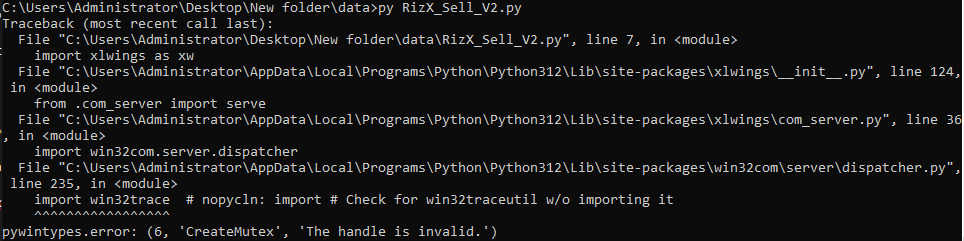

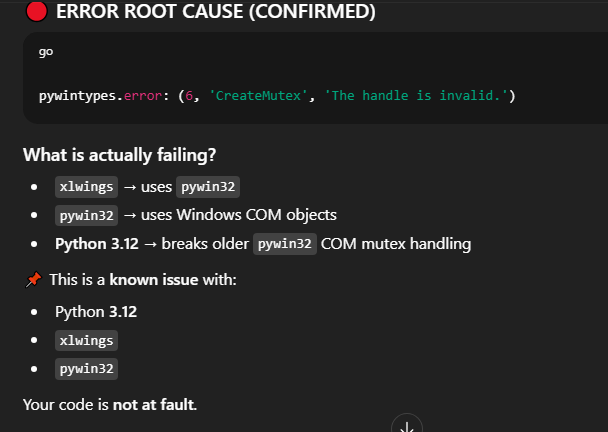

Hi TradeHull, I am unable to run my code, Its giving below error. Also while checking in ChatGPT it says. Python verison issue.

Kindly suggest, If I down grade will it work.Also I am pasting my complete code below for your reference.

Blockquote

import tradehull

import talib

import datetime

import time

import pandas as pd

import pandas_ta as ta

import xlwings as xw

import pickle

from collections import deque

from paper_patch import apply_paper_trading

===============================

INITIALIZATION

===============================

TH = tradehull.Tradehull(“”, “”, “yes”)

kite = TH.kite

apply_paper_trading(kite)

print(“\n\n”)

watchlist = [“NIFTY 50”]

single_order_status = {

‘name’: None, ‘date’: str(datetime.date.today())

, ‘entry_time’: None,

‘qty’: None, ‘sl’: None, ‘tg’: None,

‘exit_time’: None, ‘pnl’: None,

‘traded’: None, ‘combined_premium’: None,‘atm_ce’: None,

‘atm_pe’: None,

‘otm_ce’: None,

‘otm_pe’: None

}

orderbook = {name: single_order_status.copy() for name in watchlist}

===============================

EXCEL

===============================

workbook = xw.Book(‘Live Algo_Sell_V2.xlsx’)

Configuration = workbook.sheets[‘Configuration’]

live_orderbook = workbook.sheets[‘live_orderbook’]

===============================

CONFIG

===============================

reentry = “yes”

MAX_TRADES_PER_DAY = 2

DAILY_MAX_LOSS = 10000

AVG_5D_RANGE = 350

trade_count = 0

daily_pnl = 0

combined_premium_window = deque(maxlen=3) # 15 min window

day_high = -1

day_low = 10**9

def compute_underlying_context(name: str):

df = TH.get_short_length_hist_data(

name=name, exchange=“NSE”, interval=“5minute”, oi=True

)

if df is None or df.empty or len(df) < 30:

return None

df["rsi"] = talib.RSI(df["close"], 10)

df["atr"] = talib.ATR(df["high"], df["low"], df["close"], 14)

df["previous_rsi"] = df["rsi"].shift(1)

df["nifty_vol_ma"] = df["volume"].rolling(8).mean()

sqn_lib.sqn(df=df, period=14)

df["market_type"] = df["sqn"].apply(sqn_lib.market_type)

df.dropna(inplace=True)

completed_candle = df.iloc[-1]

try:

vix = TH.get_data_for_single_script("NSE", "INDIA VIX", "ltp") or 20

except Exception:

vix = 20

df["swing_high"] = dynamic_swing_highs(df, vix)

df["swing_low"] = dynamic_swing_lows(df, vix)

swing_highs_df = df[df["swing_high"]]

swing_lows_df = df[df["swing_low"]]

recent_resistance = (

swing_highs_df["high"].iloc[-1] if not swing_highs_df.empty else None

)

recent_support = (

swing_lows_df["low"].iloc[-1] if not swing_lows_df.empty else None

)

try:

df_15 = TH.get_short_length_hist_data(

name=name, exchange="NSE", interval="15minute", oi=False

)

df_15["ema20"] = talib.EMA(df_15["close"], 20)

trend_up = df_15["close"].iloc[-1] > df_15["ema20"].iloc[-1]

except Exception:

trend_up = True

return completed_candle, (recent_resistance, recent_support, df), trend_up

===============================

MAIN LOOP

===============================

while True:

current_time = datetime.datetime.now().time()

if current_time < datetime.time(9, 45):

print("⏳ Waiting for valid trading window")

continue

if current_time > datetime.time(21, 30):

print("⏹ Entry window closed")

break

if trade_count >= MAX_TRADES_PER_DAY:

print("📛 Max trades reached")

break

for name in watchlist:

live_orderbook.range('A1').value = pd.DataFrame(orderbook).T

# ===============================

# MARKET DATA

# ===============================

ltp = TH.get_data_for_single_script("NSE", name, "ltp")

day_high = max(day_high, ltp)

day_low = min(day_low, ltp)

day_range = day_high - day_low

if day_range > 1.2 * AVG_5D_RANGE:

print("🚫 Trend day detected")

continue

# ===============================

# CONTEXT FETCH (REQUIRED)

# ===============================

context = compute_underlying_context(name)

if context is None:

print("⌛ Context not ready")

continue

completed_candle, (recent_resistance, recent_support, df_ctx), trend_up = context

# ===============================

# ENTRY FILTERS (CONTEXT-BASED)

# ===============================

# 1️⃣ Market regime filter (MOST IMPORTANT)

if completed_candle["market_type"] not in ["RANGE", "WEAK_TREND"]:

print("🚫 Market not suitable (SQN)")

continue

# 2️⃣ RSI stability filter

if not (45 <= completed_candle["rsi"] <= 55):

print("🚫 RSI outside neutral zone")

continue

if abs(completed_candle["rsi"] - completed_candle["previous_rsi"]) > 5:

print("🚫 RSI momentum expanding")

continue

# 3️⃣ ATR compression filter

atr_ma = df_ctx["atr"].rolling(20).mean().iloc[-1]

if completed_candle["atr"] > atr_ma:

print("🚫 ATR expanding")

continue

# 4️⃣ Volume contraction filter

if completed_candle["volume"] > completed_candle["nifty_vol_ma"] * 1.2:

print("🚫 Volume expansion")

continue

# 5️⃣ Support / Resistance distance filter

ltp = TH.get_data_for_single_script("NSE", name, "ltp")

if recent_support and abs(ltp - recent_support) < completed_candle["atr"]:

print("🚫 Near support")

continue

if recent_resistance and abs(ltp - recent_resistance) < completed_candle["atr"]:

print("🚫 Near resistance")

continue

# ===============================

# OPTION PRICING (REQUIRED)

# ===============================

atm_ce, _, _ = TH.get_atm(ltp, name, 0, "CE")

atm_pe, _, _ = TH.get_atm(ltp, name, 0, "PE")

atm_ce_ltp = TH.get_data_for_single_script("NFO", atm_ce, "ltp")

atm_pe_ltp = TH.get_data_for_single_script("NFO", atm_pe, "ltp")

combined_premium = atm_ce_ltp + atm_pe_ltp

# ===============================

# ENTRY

# ===============================

if orderbook[name]['traded'] is None:

distance = int(combined_premium / 75) + 1

otm_ce = TH.get_otm(ltp, name, 0, distance, "CE")

otm_pe = TH.get_otm(ltp, name, 0, distance, "PE")

qty = TH.get_lot_size(otm_ce)

kite.place_order(exchange="NFO", tradingsymbol=otm_ce,

transaction_type="BUY", quantity=qty,

product="MIS", order_type="MARKET")

kite.place_order(exchange="NFO", tradingsymbol=otm_pe,

transaction_type="BUY", quantity=qty,

product="MIS", order_type="MARKET")

kite.place_order(exchange="NFO", tradingsymbol=atm_ce,

transaction_type="SELL", quantity=qty,

product="MIS", order_type="MARKET")

kite.place_order(exchange="NFO", tradingsymbol=atm_pe,

transaction_type="SELL", quantity=qty,

product="MIS", order_type="MARKET")

orderbook[name].update({

'name': name,

'entry_time': str(datetime.datetime.now().time()),

'qty': qty,

'combined_premium': combined_premium,

'sl': combined_premium * 1.22,

'tg': combined_premium * 0.82,

'traded': "yes",

'atm_ce': atm_ce,

'atm_pe': atm_pe,

'otm_ce': otm_ce,

'otm_pe': otm_pe

})

from paper_patch import send_telegram

entry_msg = (

"🟢 *NEW TRADE ENTERED_Sell_* \n\n"

f"📌 Instrument : {name}\n"

f"⏰ Time : {datetime.datetime.now().strftime('%H:%M:%S')}\n"

f"💰 Premium : {combined_premium:.2f}\n"

f"🛑 SL : {orderbook[name]['sl']:.2f}\n"

f"🎯 TG : {orderbook[name]['tg']:.2f}\n"

f"📦 Qty : {orderbook[name]['qty']}\n"

f"📊 RSI (5m) : {completed_candle['rsi']:.2f}\n"

f"📈 Day Range : {day_range:.2f}\n"

"\n⚙️ Mode: PAPER TRADING"

)

send_telegram(entry_msg)

trade_count += 1

print("✅ Trade entered")

# ===============================

# EXIT

# ===============================

if orderbook[name]['traded'] == "yes":

atm_ce = orderbook[name]['atm_ce']

atm_pe = orderbook[name]['atm_pe']

otm_ce = orderbook[name]['otm_ce']

otm_pe = orderbook[name]['otm_pe']

qty = orderbook[name]['qty']

running_ce = TH.get_data_for_single_script("NFO", atm_ce, "ltp")

running_pe = TH.get_data_for_single_script("NFO", atm_pe, "ltp")

running_cp = running_ce + running_pe

sl_hit = running_cp >= orderbook[name]['sl']

tg_hit = running_cp <= orderbook[name]['tg']

if sl_hit or tg_hit:

kite.place_order(exchange="NFO", tradingsymbol=atm_ce,

transaction_type="BUY", quantity=qty,

product="MIS", order_type="MARKET")

kite.place_order(exchange="NFO", tradingsymbol=atm_pe,

transaction_type="BUY", quantity=qty,

product="MIS", order_type="MARKET")

kite.place_order(exchange="NFO", tradingsymbol=otm_ce,

transaction_type="SELL", quantity=qty,

product="MIS", order_type="MARKET")

kite.place_order(exchange="NFO", tradingsymbol=otm_pe,

transaction_type="SELL", quantity=qty,

product="MIS", order_type="MARKET")

pnl = (orderbook[name]['combined_premium'] - running_cp) * qty

daily_pnl += pnl

orderbook[name]['exit_time'] = str(datetime.datetime.now().time())

orderbook[name]['pnl'] = pnl

print(f"🚪 Exit | PnL: {pnl:.2f}")

exit_reason = "STOP LOSS 🛑" if sl_hit else "TARGET HIT 🎯"

exit_msg = (

"🔴 *TRADE EXITED* \n\n"

f"📌 Instrument : {name}\n"

f"⏰ Exit Time : {datetime.datetime.now().strftime('%H:%M:%S')}\n"

f"📍 Reason : {exit_reason}\n"

f"💰 Entry CP : {orderbook[name]['combined_premium']:.2f}\n"

f"💰 Exit CP : {running_cp:.2f}\n"

f"📦 Qty : {orderbook[name]['qty']}\n"

f"📈 PnL : {pnl:.2f}\n"

f"📉 Daily PnL : {daily_pnl:.2f}\n"

)

send_telegram(exit_msg)

live_orderbook.range('A1').value = pd.DataFrame(orderbook).T

time.sleep(1) # allow Excel to capture exit

orderbook[name] = single_order_status.copy()

if daily_pnl <= -DAILY_MAX_LOSS:

print("🛑 Daily max loss hit")

TH.market_over_close_all_order()

break

# ===============================

# BOT SHUTDOWN CONDITIONS

# ===============================

if (

current_time > datetime.time(21, 30)

or trade_count >= MAX_TRADES_PER_DAY

or daily_pnl <= -DAILY_MAX_LOSS

):

shutdown_msg = (

"🛑 *BOT STOPPED* \n\n"

f"⏰ Time : {datetime.datetime.now().strftime('%H:%M:%S')}\n"

f"📊 Trades : {trade_count}\n"

f"📉 Daily PnL : {daily_pnl:.2f}\n"

"📌 Reason : Trading conditions exhausted\n\n"

"🤖 Status : SAFE SHUTDOWN"

)

send_telegram(shutdown_msg)

print("🛑 Bot stopped safely")

break

time.sleep(5)

===============================

SAVE STATE

===============================

with open(“orderbook_pickle”, “ab”) as f:

pickle.dump(orderbook, f)

Blockquote